As retirement plan committees take on the responsibility of managing retirement plans, they become entrusted with the financial well-being of their employees. The importance of this role cannot be overstated, and with great power comes an even greater need for stewardship. In this blog, we'll explore the key element of effective stewardship for committees overseeing retirement plans.

Stewardship follows a process-driven approach that is consistent with applicable laws and regulations, plan documents and best practices for plan management. This involves strategic decision-making, adherence to fiduciary duties, transparency and always acting in the best interests of the plan participants.

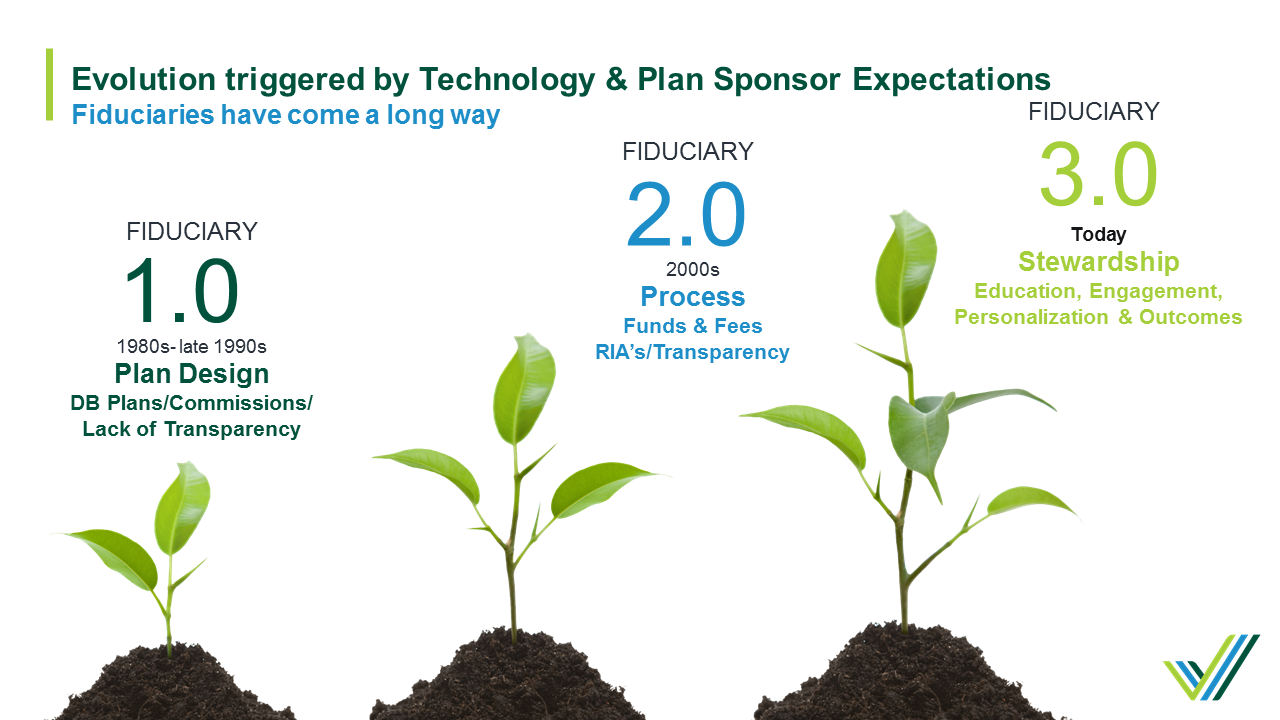

Despite its inevitability, change often happens very slowly in the retirement plan space. When considering a timeline of these shifts, we see that the first came in the 1980s into the 1990s and the second in the early 2000s, while the third has been underway for the past several years.

Despite its inevitability, change often happens very slowly in the retirement plan space. When considering a timeline of these shifts, we see that the first came in the 1980s into the 1990s and the second in the early 2000s, while the third has been underway for the past several years.

These shifts in our industry are typically preceded by technological advancements and result in different expectations from our clients.

We’re living in the early stages of what I call the “Era of Stewardship.” I’ll define Stewardship as the level of commitment an employer places on helping their employees achieve positive outcomes in retirement. This often leads to an employer making the difficult decisions of today for employees who would otherwise put such decisions off until tomorrow.

As stewards of financial well-being, committees overseeing retirement plans must adopt a strategic approach to ensure every decision and action contributes directly to the prosperity of plan participants.

Let’s delve into a few specific strategies for stewardship with a dedicated focus on enhancing participant outcomes as they relate to Plan Design.

Stewardship dedicated to participant outcomes involves continuous assessment of plan design. Committees should be proactive in responding to participant needs by adjusting auto plan features and employer contribution structures. Flexibility in plan design ensures the retirement plan evolves alongside the changing needs of participants.

Simply put, we need to auto, auto, auto everything. Let them make the decision to opt out, not opt in as most plans are currently designed. Auto features in retirement plans are essential because many participants may struggle to make optimal financial decisions on their own.

Humans are creatures of habit, and we are programmed to take the easy approach of living today, while putting off challenges until tomorrow. As a result, most of society ends up doing nothing and finds themselves left playing catch-up with their retirement saving strategy. This all changes when retirement plan committees leverage plan design to automate these challenging decisions, knowing most people will not take initiative themselves.

Automatic enrollment helps overcome inertia and increase overall plan participation by ensuring employees are enrolled in the retirement plan as the default. Similarly, auto-increase features help address the tendency for individuals to procrastinate or feel overwhelmed by complex decisions, gradually raising contribution rates over time. These features are designed to simplify the decision-making process for participants, which promotes better savings habits and enhances overall retirement preparedness.

Neglecting to use automated features may result in participants making poor decisions or – even worse – thinking decisions have already been made for them. Imagine working your entire life and thinking your company was investing in your retirement on your behalf, only to realize you forgot to set up contributions and have nothing saved. With automatic enrollments, this horror story is less likely to become a reality. Conversely, imagine automatically enrolling less engaged participants, so they build up retirement savings without even realizing.

Employers need to introduce auto features in their retirement plans to take the hassle out of decision-making for their employees and make saving as easy as possible. This feature is the helpful hand leading employees toward a more secure financial future, alleviating the stress of figuring it all out on their own.

Offering an automatic enrollment arrangement demonstrates an employer's commitment to their employees’ financial well-being. This positive approach contributes to higher employee satisfaction and retention rates, as employees appreciate your commitment to helping them build a secure financial future. Below are a few easy ways to get started in an employer’s journey towards shifting from a Plan Sponsor to Plan Steward.

Stewardship with a participant-centric focus involves setting goals that directly impact the financial well-being of individuals. Committees should work to establish realistic and measurable objectives, such as increasing overall plan participation, boosting contribution rates and facilitating personalized retirement income projections.

An easy first step after adding an automatic contribution arrangement is to deploy a contribution re-enrollment strategy and repeat it every three years. An automatic enrollment reenrollment is a process where employees who previously opted out or have a contribution rate below the automatic contribution arrangement default contribution rate are automatically enrolled or reenrolled.

The reenrollment strategy solves for the issue of inertia and promotes positive participant behavior patterns. For example, an employee early in their career may have opted out initially because they were recently married, had a baby on the way or were trying to make ends meet while saving for a home. But things change and the reenrollment strategy allows for another chance to get into the plan. Just because they opted out initially doesn’t mean saving for retirement isn’t important, perhaps the time wasn’t right then and it is now.

Employers should make sure they have a process in place to evaluate the success of the retirement plan that goes beyond traditional fee benchmarks. In collaboration with their retirement plan service providers, stewards should develop and track outcome-oriented metrics that directly reflect the participant’s financial health. This may include measuring retirement readiness, tracking income replacement ratios and assessing the success of a contribution re-enrollment strategy.

Committees overseeing retirement plans play a pivotal role in shaping the financial futures of their employees. By adopting a participant-centric approach to stewardship, focusing on personalized strategies, setting targeted goals, implementing outcome-oriented metrics, and embracing holistic financial wellness, stewards can help improve participant outcomes and strive to provide a secure and prosperous retirement for their employees.

We’ll continue the theme of Stewardship in our next blog and how this evolution is changing the landscape of participant-centric investment strategies with the concept of “Personalized Investing.”

We are here to help make retirement planning easy. Please contact your Plan Consultant or Plan Advisor if you are interested in learning more.

This website uses cookies. By accepting the use of cookies, this message will close and you will receive the optimal website experience. For more information on our cookie policy, please visit our Privacy Policy.